Build a Simple Breakout Trading Strategy in Pine Script

A breakout trading strategy is a rule-based system that enters positions when price moves beyond a defined support or resistance level. Want to automate that with Pine Script? Breakout strategies are honestly one of the best places to start. I've been testing and refining these for years, and they've taught me more about market behavior than any textbook ever did.

Here's the thing about breakouts — they're everywhere. I've seen them on AAPL, TSLA, ETH/USD, you name it. When prices finally break free from their comfort zones, momentum can carry them for days. Sometimes it's profitable momentum, sometimes... well, let's just say I've learned some expensive lessons along the way.

What Makes Breakout Strategies So Effective?

Picture this: AAPL bounces between $50 and $55 for three weeks straight. Every time it hits $55, sellers step in. Every time it drops to $50, buyers jump in. Then one morning, boom! It smashes through $55 like it's nothing and rockets to $60.

That's a breakout in action. The beauty is that these patterns repeat constantly across all timeframes and markets. When enough buying or selling pressure builds up, prices don't just nudge past resistance — they often explode through it.

The psychology behind this is fascinating. Traders get comfortable with ranges. They expect the bounce. But when that expectation gets shattered, panic buying (or selling) kicks in, creating momentum that can last for days or even weeks.

Building Your First Pine Script Breakout Strategy

Let me walk you through how I approach coding these strategies. The core concept is beautifully simple, but don't let that fool you — simple often works best in trading.

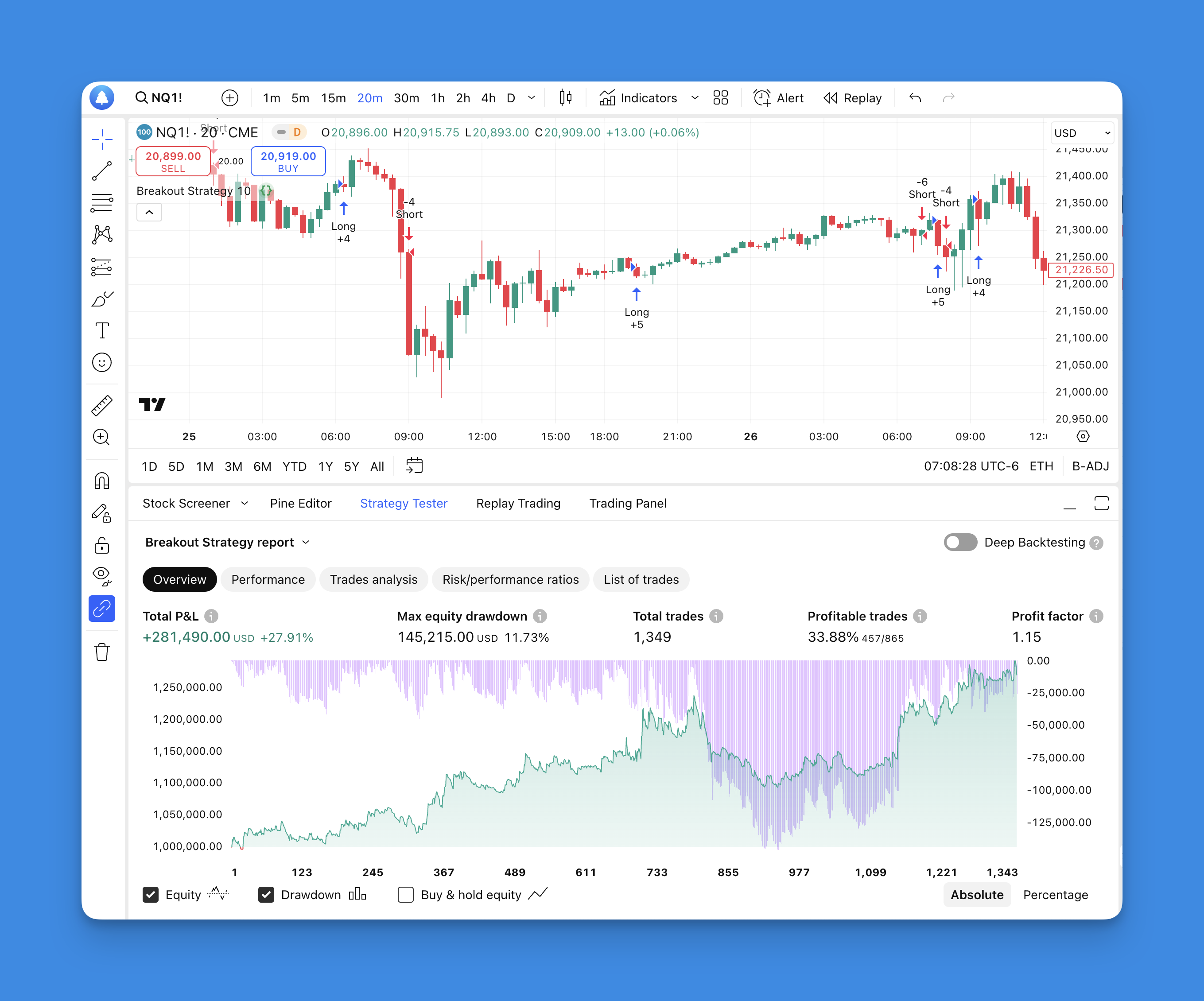

Step 1: Define Your Trading Range I track the highest high and lowest low over a specific period. Think of it as drawing a box around recent price action. Most traders use 20 periods as a starting point, but I've seen everything from 10 to 50 work depending on the market and timeframe.

Step 2: Watch for the Break When price punches above yesterday's high point, that's our signal to go long. When it crashes below yesterday's low point, time to go short. The key word here is "yesterday's" — we always use the previous bar's levels to avoid repainting issues.

Step 3: Execute the Trade This is where Pine Script shines. Once our conditions are met, the strategy automatically enters positions without any emotional interference from us humans. I've found that keeping exit rules equally mechanical is just as important — my stop goes just below the breakout level, and I trail it as price moves in my favor.

The Complete Pine Script Code

Here's the working code I use. Don't worry if you're new to Pine Script — I'll break down what each section does:

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Pineify

//======================================================================//

// ____ _ _ __ //

// | _ \(_)_ __ ___(_)/ _|_ _ //

// | |_) | | '_ \ / _ \ | |_| | | | //

// | __/| | | | | __/ | _| |_| | //

// |_| |_|_| |_|\___|_|_| \__, | //

// |___/ //

//======================================================================//

//@version=6

strategy("Simple Breakout Strategy", overlay=true)

// How many bars back do we look for our highs and lows?

length = input.int(title="Lookback Period", minval=1, maxval=1000, defval=20)

// Find the highest high and lowest low over our lookback period

upBound = ta.highest(high, length)

downBound = ta.lowest(low, length)

// Enter long when we break above the previous bar's upper bound

if (high > upBound[1])

strategy.entry("Long", strategy.long)

// Enter short when we break below the previous bar's lower bound

if (low < downBound[1])

strategy.entry("Short", strategy.short)

This code is deceptively powerful in its simplicity. The ta.highest() and ta.lowest() functions do the heavy lifting, constantly updating our trading range. The [1] notation ensures we're using historical data, not current bar data that could change.

Why Breakout Strategies Actually Work (When They Do)

Let's be real — no strategy works 100% of the time. But breakouts have some genuine advantages:

Early Trend Detection: You're often catching the very beginning of significant price moves. While other traders are still debating whether it's a "real" breakout, you're already positioned.

Clear Risk Parameters: Your stop loss is obvious — just below the breakout point for longs, just above for shorts. No guesswork involved.

Scalability: This strategy works across different markets and timeframes. I've used variations on everything from 1-minute scalping to weekly position trades. I prefer the 1-hour crypto markets myself — the balance of signal quality and frequency works better for my schedule.

Psychological Edge: You're trading with momentum, not against it. When prices break out, you're riding the wave instead of trying to catch falling knives.

Advanced Optimization Techniques

After running thousands of backtests, here are the modifications that actually moved the needle:

Volume Confirmation: I only take breakouts when volume is at least 150% of the 20-period average. Fake breakouts on low volume are the devil. You can learn more about implementing volume analysis in this Pine Script volume footprints guide.

Multiple Timeframe Analysis: Check if the higher timeframe trend aligns with your breakout direction. If you're new to this concept, this multi-timeframe Pine Script guide will open your eyes to a whole new level of analysis.

Dynamic Stop Losses: Instead of fixed percentage stops, I use ATR-based stops that adapt to market volatility. The ATR strategy guide explains how to set this up properly. This approach has saved me from getting stopped out during normal market noise countless times.

Filter Out Noise: Add a minimum breakout distance. If the breakout is only a few cents, it might not have enough momentum to sustain itself.

Common Mistakes That'll Cost You Money

I've made every mistake in the book, so learn from my pain:

Testing on Limited Data: Backtest over multiple market conditions — bull markets, bear markets, sideways chop. What works in trending markets often fails miserably in range-bound conditions. I backtested a version of this on BTC/USD 4-hour candles from 2021-2023 and got completely different results across bull and bear phases.

Ignoring Transaction Costs: Those small commissions and spreads add up fast, especially on shorter timeframes. Make sure your average win is significantly larger than your costs.

Over-Optimization: Just because changing your lookback period from 20 to 19 improves your backtest doesn't mean it'll work going forward. If you're serious about strategy development, check out these Pine Script v6 strategy examples for inspiration.

No Position Sizing: Risk management isn't optional. Never risk more than 1-2% of your account on any single trade, no matter how "sure" you are.

Building Strategies Without Coding

Look, not everyone wants to spend months learning Pine Script syntax. I get it. That's why tools like Pineify are popular with traders who have ideas but limited coding time.

With Pineify, you can drag and drop conditions to build breakout strategies without writing a single line of code. You combine multiple indicators, set complex entry and exit rules, and add filters — all through a visual interface.

The platform handles all the technical stuff like avoiding repainting, managing position sizing, and optimizing for different timeframes. Plus, it generates clean, readable Pine Script code that you can study and learn from.

I'll be honest though — I don't think visual builders replace understanding the logic underneath. If you don't know why your stop loss sits where it does, a drag-and-drop interface won't save you. I've also found that complex multi-condition strategies can get messy in visual builders faster than they do in raw code. So start simple either way.

Website: Pineify

The Reality Check

Here's what nobody tells you about breakout strategies: they're brutally honest about market conditions. In strong trending markets, they'll make you feel like a genius. In choppy, range-bound markets, they'll humble you real quick.

The key is understanding when to use them and when to step aside. I've learned to avoid breakout strategies during major economic announcements, low-volume holiday periods, and when volatility is extremely low.

Also, remember that past performance doesn't guarantee future results. That's not just legal disclaimer nonsense — it's the cold, hard truth of trading. Markets evolve, and strategies that worked five years ago might not work today.

Taking Your Strategy to the Next Level

Once you've mastered the basic breakout concept, there are endless ways to improve and adapt:

Add Fundamental Filters: Only trade breakouts in stocks with strong earnings, growing revenue, or positive analyst sentiment.

Combine with Technical Indicators: Use Bollinger Bands to identify when prices are compressed and ready to explode, or RSI to avoid buying overbought breakouts.

Sector Rotation: Focus on breakouts in sectors that are currently in favor. A breakout in a strong sector has better odds than one in a lagging sector.

News-Based Triggers: Some of the best breakouts happen around earnings announcements, FDA approvals, or major product launches.

Breakout strategies aren't about being right all the time. I've taken plenty of losses — my win rate on the basic version hovers around 32-35% across most markets. But when I win, the average move is about 2.5x my average loss. That's the math that keeps me coming back. Start simple, test thoroughly, and add complexity as you gain experience.

What lookback period should I use for a Pine Script breakout strategy?

I usually start with 20 bars, but I've gone as low as 10 and as high as 50 depending on the market. Shorter periods give you more signals but more fakeouts too. Longer periods give you fewer trades but the quality tends to be better. You really need to test several values across different market conditions before committing to one.

How do I avoid repainting in a Pine Script breakout strategy?

Use the [1] index notation to reference the previous bar's highest high or lowest low rather than the current bar. In the example code, upBound[1] and downBound[1] make sure entry conditions are evaluated on confirmed, closed-bar data instead of values that can change within the same bar. I've seen traders skip this and wonder why their backtest results don't match live trading.

How can I add volume confirmation to filter fake breakouts?

Calculate a rolling average volume with ta.sma(volume, 20), then only allow entries when the current bar's volume exceeds 150% of that average. Add the condition to your if block like this: if (high > upBound[1] and volume > ta.sma(volume, 20) * 1.5). This single filter will cut your whipsaws significantly. I haven't tested this on every market, but it works well on liquid large-cap stocks and major crypto pairs.

What is an ATR-based stop loss and why use it in breakout strategies?

An ATR (Average True Range) stop loss sets your exit distance as a multiple of recent volatility rather than a fixed percentage. For example, placing a stop 1.5 x ATR below the breakout entry adapts to current market noise and avoids premature exits during normal price swings. I prefer this over fixed-percentage stops because it accounts for the actual volatility of whatever instrument you're trading.

Can I use this breakout strategy on crypto and forex, not just stocks?

Yes. Since the strategy is based purely on price levels (highest high and lowest low), it works on any liquid instrument including crypto pairs, forex majors, and futures. I'd adjust the lookback period and add an ATR-based stop to match the higher volatility typical in crypto and forex. I haven't tested it on exotic forex pairs though — the spreads there might eat you alive.

How do I backtest a breakout strategy in Pine Script without overfitting?

Test across at least two to three years of data covering bull, bear, and sideways conditions. Avoid tweaking parameters until you see consistent results, then validate on an out-of-sample period you did not optimize on. I also make sure to account for realistic commissions and slippage in the strategy() declaration — otherwise your backtest numbers will look way better than reality.